Attention to Details Pays Off

Attention to Details

On Monday, I shared the song, All the Small Things, as a reminder to pay attention to financial decisions both large and small. I truly believe that when you focus on the small things, you are building good money habits that lead to a better decision making process across the board. In addition to focusing on details, though, you need to actually pay attention to the details of your financial life.I have spoken about it here, wrote about it in my book, and I tell clients all the time that they need to schedule time to review various aspects of their financial picture. We are all busy and rarely stop to slow down and pay attention to the details; however, when we don’t pay attention to the details, we put our financial health at risk and prevent positive change from taking place.

Client Success Story

I LOVE my job! I literally have the greatest job on the planet. I get to help people understand their money and achieve their goals and dreams because they understand their money. There really is nothing better than having a front row seat to the success story of a client. Seeing my clients achieve their goals is the greatest high I can imagine.So, let me tell you about this one, for anonymity’s sake, we will call her Gretchen. I met Gretchen through a mutual friend in January of this year. Here are some of her financials when I met her:

Gretchen's Financial Snapshot - January 2014

Salary: $55,000Credit Card Debt: $2,000Student Loan Debt: $75,000Total Savings: $630Credit Score: 645 – Fair to Average

Gretchen’s Goals

Gretchen has a number of things she wants to accomplish in life; however, her immediate concerns are building up her savings and potentially buying a car in the near future. She has a used car, but it is old and will eventually need to be replaced. Her longer term goal is to buy a home, and of course pay off her student loans. She works for a non-profit, though, and is eligible for the loan forgiveness program, so we have not prioritized an accelerated student loan repayment plan.When I looked at Gretchen’s overall financial picture, my biggest concerns were the fact that she didn’t have enough saved in her emergency savings account should something unforeseen happen and her credit score would hurt her more than help her should she need to finance her replacement car. Therefore, when I put together Gretchen’s plan, I emphasized savings and credit repair as two key areas for her to work on.

Gretchen’s Plan

We pulled Gretchen’s credit report immediately, and she discovered that there was a credit card on her profile that belonged to her parents. It actually had a high utilization rate (which is not good for your credit score), and Gretchen did not even use the card, so she called the card company and had her name removed from the account. She also only had one credit card with a $2,000 limit on it, so we discussed the possibility of applying for another card once her credit score improved so that her utilization rates and credit available (both factors in credit scoring) would improve.As far as the savings plan, we determined the amount that she would auto-draft to her savings account every month, and we also created a separate travel savings account because we knew she liked to travel and also had some upcoming weddings. In addition to the savings, we discussed that she should also be saving the estimated amount of a car payment. She does not have a car payment now, but she will likely have one in the future and a good way to not only save for a down payment for a car, but also know that you can afford a car payment is to pretend like you already have the payment. The monthly pretend car payment can go to a separate savings account for your future car.

Gretchen’s Results

A month ago, Gretchen applied for another credit card and was approved for $5,000. Her picture now looks like this:

Gretchen's Financial Snapshot - September 2014

Salary: $55,000Credit Card Debt: $700 (she pays this off monthly in full)Student Loan Debt: $72,000

Total Savings: $6,091

Credit Score: 763 – EXCELLENT!!!!!!!!!

Loan Savings

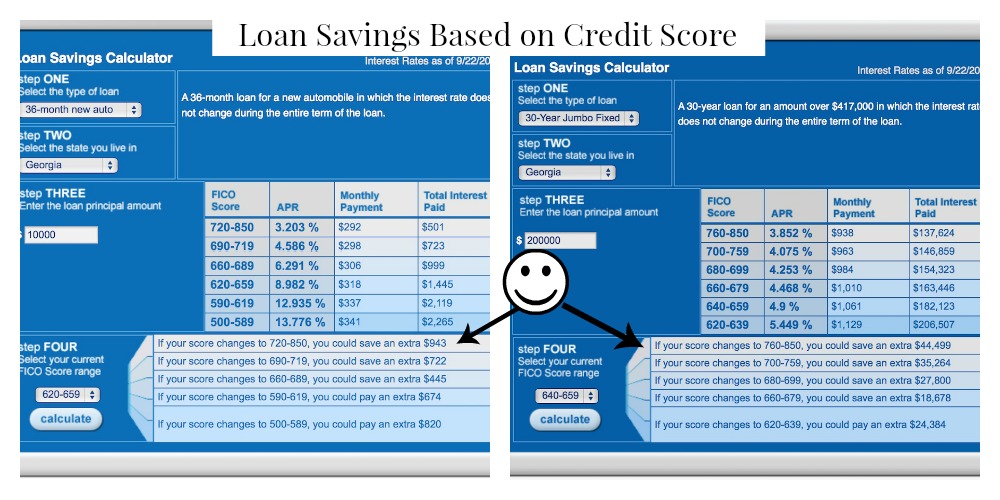

In nine months, Gretchen went from $630 in savings to $6,091. She went from $2,000 in credit card debt to $700, and her student loan debt decreased by $3,000. However, the most exciting stat for me is the fact that she improved her credit score from 645 which is fair or average to 763 which is excellent!! Why do I care so much?Because I know that Gretchen will need financing in her future to help her achieve her goals of buying a car and eventually owning a home. Now that she has improved her credit, she will save an expected $943 on her car financing over 3 years, but more importantly $44,499 in her mortgage over 30 years. *Analysis Source: MyFico.com

*Analysis Source: MyFico.com

Investment Returns

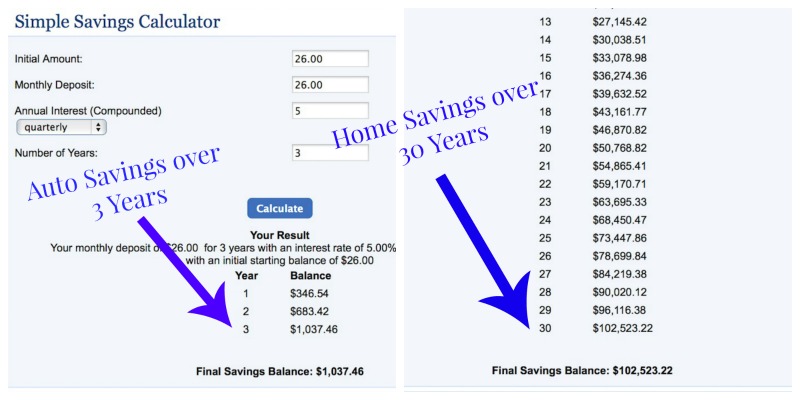

Rather than just looking at the savings, I like to look at the potential of the savings. If Gretchen chooses to take her savings and invest it (which I would encourage her to do) into a simple bond fund or ETF, assuming a 5% return over time and interest compounded quarterly, Gretchen has the potential to EARN $1,037 on her car savings and EARN $102,523 on her home savings.By paying attention to the details and working on her financial health, Gretchen changed the course of her finances and now achieving her dreams is not only a likelihood, but she is going to do it and save money along the way, allowing her to dream up even greater goals. *Analysis Source: Bankrate.com

*Analysis Source: Bankrate.com

Do you check your credit score regularly? Have you seen changes to your finances based on attention to detail?

PS: If you would like to work with me, check out my company site, Next-Gen Financial for more details Image Source: FreeDigitalPhotos.Net Stuart MilesGif Source: Giphy